If you don’t have a bank account yet, you should open one. (Continue reading for some suggestions.) Anyone who earns money from a job or any other source — even if there isn’t a lot of money to spare — should be using a checking account at the very least.

My bank tells me I’ve been a customer since the year I turned 13, so whether it was from an allowance, from taking care of my neighbor’s cat while they were on vacation, or from my first job in retail, I was at least trying to have a positive money attitude, inspired by my parents.

It’s possible to be successful without a bank account, but without one, you’ll have obstacles in today’s society. You can work at a job where you’re paid cash, or you can use check-cashing services at Walmart or storefronts. Prepaid debit cards can help you buy things in an increasingly cashless environment. But all these workarounds are expensive and limit your financial possibilities.

Bank accounts can be expensive, too, and many of these financial corporations will try to fleece you at any opportunity with overdraft fees, minimum balance requirements, maintenance fees, and ATM fees. The list of hidden fees seems to go on forever. Avoiding fees sometimes requires some attention, but when you can, checking and savings accounts are much better than “alternative banking products.”

You don’t need to go crazy. You can do everything you need with one checking account, but to make the most out of benefits banks have to offer, you’d need one savings account as well. That will help you earn interest on the money of yours you let the bank use — yes, when you deposit money in a bank account, you’re letting the bank use your money, so they should be giving you something in return (in addition to your ability to withdraw any amount of your money at any time).

I prefer the KISS strategy when it comes to bank accounts: Keep It Simple, Stupid. (No offense.)

Choose one of these best bank accounts to open.

Best Overall Bank Account for an Adult.

Fidelity Cash Management Account. This is the best example of the KISS method of banking. It’s a checking and a savings account in one, though the amount of interest you earn is minimal. But for a primary bank account, that’s just fine. Everything is free. Let me repeat: Everything is free. There’s no minimum balance. When you want to use an ATM, the owners will charge a fee, but Fidelity pays you to cover that fee.

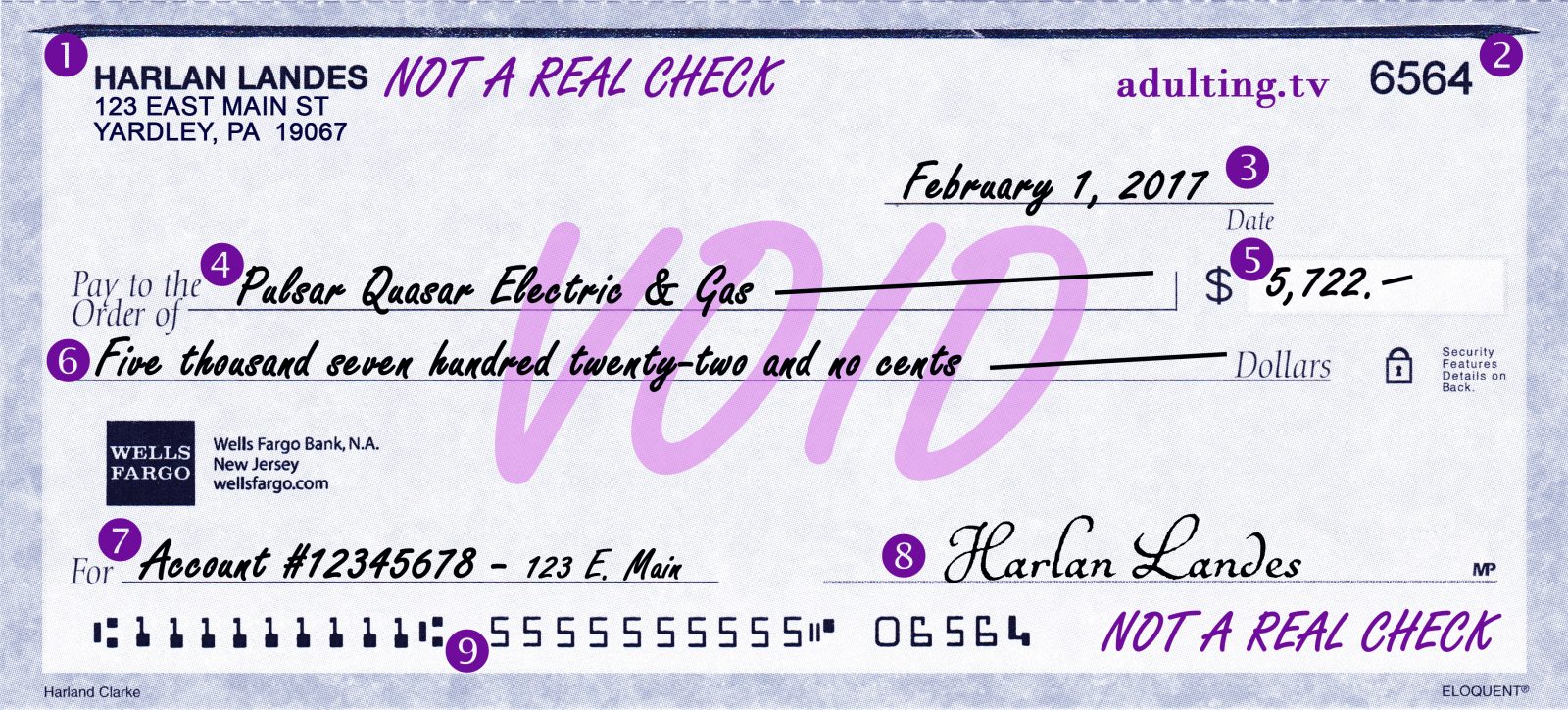

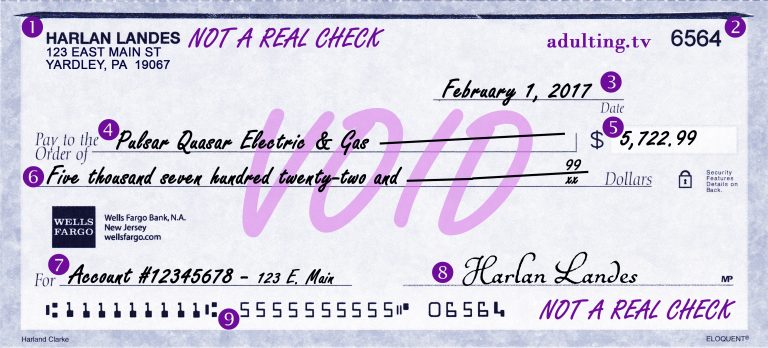

You receive free checks to use. (You should learn how to use a checkbook and how to write checks if you don’t already know.) You can deposit any checks you receive using an app on your phone. Of course, you receive a debit card to access your money using an ATM or for purchases. Open a Fidelity Cash Management account.

Best Bank Account for an Adult Who Doesn’t Trust Banks.

Your local credit union. Not a fan of the financial industry? Credit unions don’t answer to Wall Street, so they’re not always trying to profit from their customers. Credit unions are owned by their members (who are also their customers), so it’s a system that makes the needs of the customers their priority.

Many community credit unions are open to anyone, but some have restricted membership. Navy Federal Credit Union is one of the best-reviewed credit unions out there, but you need to be affiliated with the military or the Department of Defense (or have an immediate family member who is) in order to join.

The Navy Federal Credit Union e-Checking is that organization’s best option taking all the facets of banking into account.

An independent credit union may also be the best option for Socially Conscious Adults. (Trump fans should head to CitiBank or Wells Fargo; the president owns stock in these companies.) Search for a credit union.

Best Bank Account for an Adult With Limited Mobility.

The branch that’s local to you. For a while in my adult life, I didn’t own a car. That really limited my ability to get around to a distant branch. This might apply to someone who lives in a walk-able city, too, like New York City.

Convenience is an important factor in choosing a bank account, sometimes more than a tiny bit of interest you might earn. So if you have a bank within a walking distance of 60 seconds, no one would ever judge you for choosing that bank’s free checking option over another bank.

Almost every bank account in existence today can be managed online, so there should be very few things you need to actually travel to a branch for. But sometimes, something comes up. But any online account should also be good for someone without access to transportation. Ally Bank is a strongly-reviewed online bank with a standard checking account. Simple is another interesting choice.

Best Bank Account for Adults Who Earn Interest.

Synchrony High Yield Savings. If you want just one bank account, choosing a checking account like one of the above. If you’re ready to have both a checking account and a savings account, and you’re moderately good at managing your money, a high yield savings account is a good choice for a second bank account.

And in recent years, Synchrony has offered one of the highest interest rates around. As of right now, that’s 1.05% APY (annual percentage yield). What does that mean? If you deposit $1,000 on day one and do nothing else, on day 366, your balance will be $1,010.50.

Not a huge increase, but it’s better than ending up with less. And we’ve been at a low point in interest rates. They will rise in the future — we just don’t know when. Open a Synchrony High Yield Savings account.

Best Bank Account for Adult Entrepreneurs.

Citizens Bank Clearly Better Business Checking. It’s important to separate your business finances from your personal life. If you develop a business, or you start earning money from your hobby in a serious way, you’ll want a business checking account. Make your business official with the state and federal governments, then open this account.

There are no maintenance fees and no minimum balance requirement, so it’s perfect for your side hustle. The bank offers 200 free check transactions, which should be sufficient for most small businesses. Open a Clearly Better Business Checking account.

![[A045] Ish Happens: Prepare For the Inevitable Emergency](https://adulting.tv/wp-content/uploads/2016/11/a045-1200x628.jpg)