Once in a while, we present Adulting.tv LIVE! Stay tuned to hear about future events, and share your questions about or suggestions for our next discussions!

Is it possible to earn money AND do what you love? Even if you’re able to figure out what your passion is, do you really believe that if you pursue your passion the money will follow? Sometimes, it’s possible, but not always the same way motivational speakers lead to you believe. Pursuing your passion is important, and possible, but earning a living may be related to your passion and it may not be.

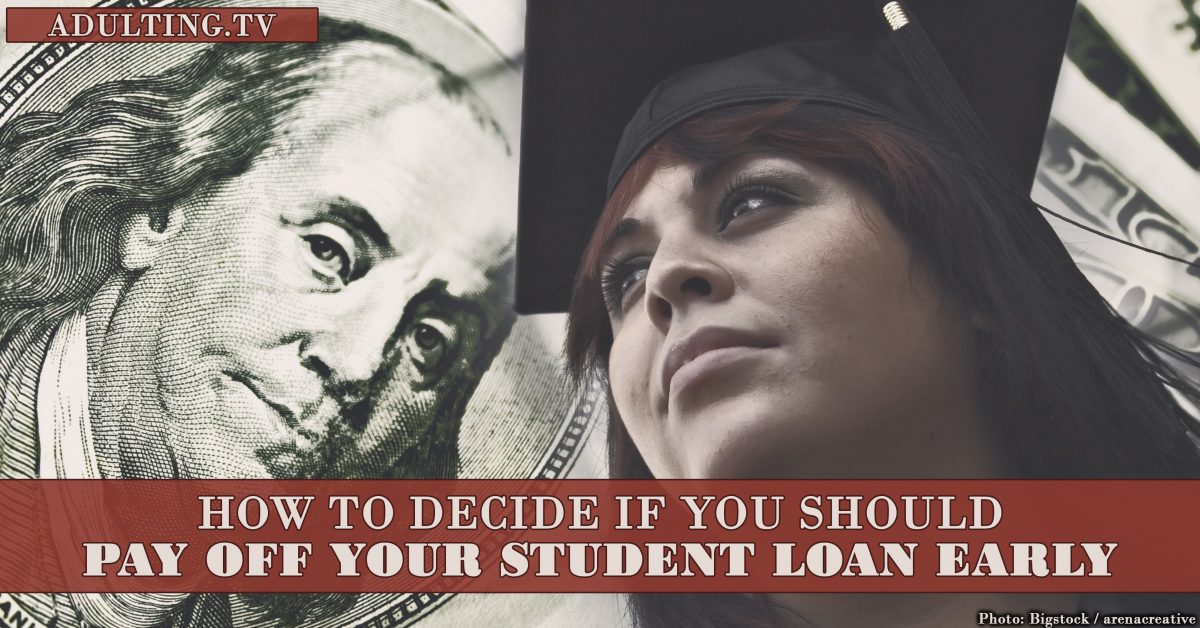

When I first started my career as a freelance writer and financial expert, my main selling point was the fact that I had paid off my student loans early.

I did it in three years.

While I’m still proud of that accomplishment, I did it because that was the best decision for me. That doesn’t mean it’s the best decision for everyone.

There are plenty of factors that could have made my debt strategy pointless – or even downright harmful. I constantly meet and consult with people who would be better off paying their student loan debt down at a slower rate.

But how can you tell which camp you fall in? Here’s what you need to know about paying off your student loan:

When you shouldn’t pay off your student loan early.

There are times it just doesn’t make sense to pay off your student loan early. It seems like a lot of the advice is to get rid of the debt as fast as possible, but here are some reasons to think twice:

If you have other debt. Student loan debt typically comes with lower interest rates than other forms of debt. Plus, the interest is deductible on your taxes.

It’s better to pay off credit card debt or other high-interest loans before focusing on student loans. Once those high-interest loans are paid off, pay off any loans with comparable interest rates, since they’re unlikely to offer the same tax benefits as the student loans.

If you qualify for a forgiveness plan. Anyone who qualifies for a loan forgiveness plan through the federal government or other organization, such as the Public Service Loan Forgiveness program, should make the smallest payments possible on their loan — especially if they won’t owe taxes on the forgiven debt.

If you’re in this situation and pay more than you have to every month, you’re just throwing money away.

If you don’t have an emergency fund. Paying extra on your student loans only makes sense if you already have an emergency fund in place. An emergency fund allows you to pay cash for crises like car accidents or hospital stays, and without one you may have to use a credit card or high interest loan. Save at least $1,000 for an emergency before putting extra money on your student loans.

An emergency fund allows you to pay cash for crises like car accidents or hospital stays. Without emergency savings, you may have to use a credit card or high-interest loan. Save at least $1,000 for an emergency before putting extra money on your student loans.

If you have a low interest rate. Many people only make the minimum payments on their student loans if they have a low interest rate.

Instead of putting extra money toward their debt, they can earn a higher return by investing that money in the stock market. It might seem crazy to willingly carry debt, but the math could work out in your favor. For example, students who took out federal student loans after 2016 have a 3.76% interest rate, while many index funds have an average 10% rate of return.

It might seem crazy to willingly carry debt, but the math could work out in your favor. For example, students who took out federal student loans after 2016 have a 3.76% annual interest rate, while many index funds have an average 10% annualized rate of return.

Investing isn’t a sure thing, though, so make sure you think it through before taking the plunge.

If you aren’t saving for retirement. Saving for retirement should be the most important financial priority for anyone, including millennials and Gen Z.

Paying off your student loans early is a valiant goal, but it shouldn’t distract you from saving enough for your golden years. You should be saving between 10% and 15% of your income for retirement before you even consider putting extra cash towards your student loans.

When you should pay off your student loan early.

There are definitely times that you need to tackle those student loans right now, and pay them down as quickly as possible. Here are some of the times you can feel free to demolish your debt as quickly as you can:

If you don’t have other financial obligations. There are very few reasons not to pay off your student loans early if you’re already saving for retirement and are otherwise debt-free. Paying your student loans off early could save you thousands in interest – and make it easier to save for other goals like a vacation abroad or a new car. Being debt free will also increase your credit score and make it easier to apply for a mortgage, business loan or rewards credit card.

Paying your student loan off early could save you thousands in interest – and make it easier to save for other goals like a vacation abroad or a new car. Being debt free will also increase your credit score and make it easier to apply for a mortgage, business loan or rewards credit card.

Being debt free will also increase your credit score and make it easier to apply for a mortgage, business loan, or rewards credit card.

If you have a high interest rate. When I graduated and started paying my student loans, my interest rate was 6.8%. That rate is comparable to what I could’ve earned if I invested my money in the stock market. In that instance, paying off my student loans and saving on interest made more mathematical sense. I saved more than $5,000 in interest by paying off my loans early.

In that instance, paying off my student loans and saving on interest made more mathematical sense. I saved more than $5,000 in interest by paying off my loans early.

If you get anxious about your debt. A study published in the European Journal of Public Health found that adults with debt suffered from significantly more mental health issues than those without.

It’s not surprising, given the omnipresent weight that debt represents. Debt can cause constant pressure. You feel the nagging at the back of your brain. Paying off your student loans earlier can relieve anxiety, stress, and depression, plus increase your quality of life and stifle that subconscious negativity.

If you want to switch careers or start your own business. Not having to pay on your student loan every month frees up your budget for other things. It allows you to switch to a low-paying job you love or even become self-employed.

Becoming debt free faster means you can gamble on your salary without the risk of missing payments or defaulting on your loans.

Where do you stand? Are you aggressively paying your student loan early? Or are you taking it slow?

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

Let’s be honest: when we talk about being a cheap holiday Grinch, it’s about the money. The good news is that you can spread holiday cheer without breaking the bank. Read More...

As an adult, you need to realize that you have responsibilities to others. During the holidays, society expects you to give to others and tips a little extra. You don’t want to be the cheap holiday Grinch that others despise.

We take a look at giving, how to properly tip, and what it means to spread holiday cheer.

Our Do Nows help you identify who needs a tip, as well as strategies to help you enjoy the holidays without breaking the bank.

Concepts

The realities of holiday tipping in our society.

Who should you be tipping? And how much should you give?

What makes you a cheap holiday Grinch?

How to enjoy time with family and friends during the holidays without spending more than you can afford.

Tips for writing a holiday note or card to add extra holiday cheer.

How to maintain relationships throughout the year.

Become a Friend of Adulting

To get Adulting delivered directly to your device, subscribe using Apple Podcasts, Stitcher, Google Play, or your app of choice.

Broke AF? Worried about your debt? You might think you can’t invest, but maybe you can. Here’s how to decide what step to take next on the road to financial freedom. Read More...

This week, we talk about the considerations that come when trying to decide whether or not to start investing when you still have debt.

Concepts

The importance of investing.

Ways debt can slow you down.

Are you really ready to invest?

Can you balance paying down debt with investing?

Have you taken care of other areas of your finances, like an emergency fund?

Tips for making investing more effective.

How to decide if it makes sense to invest instead of pay down debt early.

Different types of debt and which you should tackle first.

The importance of being able to sleep at night.

Don’t forget to listen to our “Do Nows” this week. We’ll take a look at how to create a debt payoff plan, open an investment account, and assess how much you need to start saving today to hit your retirement goals.

Become a Friend of Adulting

To get Adulting delivered directly to your device, subscribe using Apple Podcasts, Stitcher, Google Play, or your app of choice.

One cannot deny that a good spirit uplifts the spirit. As the saying goes, “alcohol doesn’t solve problems, but neither does milk.”

Sometimes a good drink feels good or makes the good great.

It takes the balancing skills of a cocktail server to enjoy just a few drinks, though.

One’s never enough. Two or three are perfect.

After two drinks or three drinks, though, your smartest brain cells go full-Kanye. By morning, you’re bound to have done or said something you regret.

Another saying goes, “Hindsight is 20/20.” As I have lots of hindsight, let me show you the way as we determine how many drinks is too many.

You’ve had enough to drink when you think texting your ex is a good idea.

Even if you can text an intelligible sentence, there’s likely nothing you will text an ex with the loose tongue of the turnt and burnt that will improve relations with your former relation.

You’ve had enough to drink when you forget what year it is and you think calling your ex is a good idea.

The only person who ever benefited from calling an ex is Adele.

You are not Adele.

Alas, none of us can be Adele. It’s a harsh reality we all must deal with – that and that contacting an ex is rarely a good idea.

You’ve had enough to drink when you think “calling out” your friend is a good idea.

How many drinks is enough? Well, what are you about to say to your friend?

It’s never a good idea to have a few drinks and then “get real” with your BFF. If this emotion builds inside you after kicking back a few, there are clearly issues to address. The further away from your last drink, the better you address those issues.

You’ve had enough to drink when it takes you three days to recover.

While your tolerance to alcohol may not change as you age, your tolerance for drinking does. Sorry, friends, a fatty liver can only withstand so much.

As you age, hangovers hang longer and longer, making it harder and harder to adult. If you notice a pattern of nighttime partying thwarting daytime adulting, you need to ask yourself how many drinks you should really be having — and maybe cut back.

You’ve had enough to drink when going to Denny’s sounds “awesome.”

If you’ve had enough drinks to think that going to Denny’s belongs on the ongoing list of 1,000 awesome things, you’ve had enough.

Unless you’re going to a Chinese restaurant, if you start heading toward a restaurant with pictures on the menu, start heading home.

You’ve had enough to drink when Taco Bell sounds like a healthy alternative to Denny’s.

Pictures on a menu notwithstanding, if you think a 7-Layer Burrito sounds like a healthy alternative to a Denny’s Triple Stack, you’ve had enough.

If you’re that hungry, go home, eat whole wheat bread with honey, down two aspirin and a pint of water and go to bed.

You’ve had enough to drink when you think a 2 a.m. visit to the ATM is a good idea.

As Chris Rock so wisely opined, “There’s never a good reason to be at an ATM at two in the morning!”

No matter how good your conceived plan that justifies an early morning ATM-stop, you’ve had too much.

Keep driving until you get home. Do not pass go and do not collect $200.

You’ve had enough to drink when you need a “kick stand.”

How many drinks is too many? When you start approaching it from the other end. Do you need a “pick-me-up” to put yourself down? Like adding letters to math, one problem doesn’t make the other easier.

You’ve had enough to drink when you’re the last one standing.

Being the last one standing is often a reasonable goal. Such is victory in war or soccer or family dinners. When you’re the last one at the bar or party and you’re still slinging a few back, you’ve had enough.

You’ve had enough to drink when you start reenacting scenes from Jackass.

Drinking causes the loss of cognitive reasoning. When it seems reasonable to perform stupid human tricks, it’s reasonable to think that you’ve had enough to drink.

You’ve had enough to drink when the street looks like a comfortable place to lie down.

It’s a law of physics that the more you drink the lower your center of gravity. If your center of gravity gets so low that it’s physically impossible to not lie on the ground, bar booth, or your Uber driver’s back seat, you’ve had too much to drink.

You’ve had enough to drink when you steal random street signs or event decorations.

If, in the morning, you wake and there’s a street sign waiting for a spot on your wall, or if there’s a life-size Samuel Adams sitting in your living room, you had too much to drink last night. It’s time to re-evaluate your life choices — and how many drinks is enough.

You’ve had enough to drink when your dance moves include moves you typically wouldn’t even do with the most intimate partner.

If you think you’re reinterpreting Dirty Dancing or twerking with strangers, you’ve had too much to drink. If going to bed isn’t an option, at least go sit in the corner, baby.

You’ve had enough to drink when you become richer the more you drink.

Everyone likes to be the life of the party and the easiest way to become the life of the party is to pay for the party. If you catch yourself increasingly saying, “This round’s on me!” you’ve had too much to drink.

You’ve had enough to drink when Amazon makes deliveries you don’t remember ordering.

Late night shopping with a bottle of wine and Amazon Prime is fun. And it beats watching reruns of The Gilmore Girls.

Unfortunately, there are a lot of myths surrounding investing. It’s easy to be intimidated by investing when you think about the jargon and you’re concerned about what the stock market is doing.

Before you assume that investing just isn’t for you, get the full story. Here are five investing myths keeping you from leveling up with your money:

First, you can open an investment account with many brokers with $0. Many brokers will let you invest between $50 and $100 a month if you sign up for an automatic investing account.

There are even startups, like Acorns, that allow you to invest your pocket change. Use dollar-cost averaging to start investing consistently. Eventually, you’ll want to boost the amount you invest each month. But the important thing is to start investing early.

2. I don’t have enough assets to get help investing.

Many of us feel more comfortable when we have someone to help us make investing choices. Sadly, there are money managers that do require you to have a lot of assets before they will even look at you.

But that doesn’t mean you’re out of luck.

Thinking that you need a human person dedicated to your investment management is one of the biggest investing myths. Get over it and embrace the technology available to us.

The rise of robo-advisors can be a great help to anyone with few assets and a desire for a little direction. You won’t get personalized help from robo-advisors, but you will get an idea of how to start, and someone else to guide you.

If you want a little more personalized direction, but don’t have the asset count for someone to straight manage things for you, consider a fee-only financial planner. At the very least, one of these folks will help you create a map for the future for a flat fee.

3. I need to understand how to pick stocks.

Honestly, you shouldn’t go anywhere near stock picking until you have a little experience with investing.

When you start investing, it makes more sense to start with index mutual funds and ETFs. These are groups of investments that have something in common. Personally, I prefer all-market index funds that follow everything publicly traded on U.S. exchanges. I also like S&P 500 funds because they offer access to a wide swath of the market.

Index funds and ETFs allow you take advantage of overall market performance rather than relying on your ability to get it right with a few individual stocks. Over time, the market generally goes up; it’s never gone negative in any 25-year period.

Start with funds. Learn a little. Get your feet wet. If you still want to pick stocks later, use not-for-retirement money to experiment.

4. I have to know how to “win.”

Do you have a competitive nature? If so, you might be tempted to think that you have to beat the market.

While it’s fun to think you can outperform the market, it’s foolhardy to focus on such a goal. Investing myths lead you to believe that it’s not worth it unless you’re “winning” against someone.

The truth is that you don’t need to be better than anyone. You just need to focus on your own goals. Stop worrying about how your friends invest. Don’t tie your self-worth to whether or not your portfolio does better than the market.

You don’t need a portfolio that’s bigger than someone else’s.

What you need is a plan to meet your personal financial goals.

Rather than obsessing over whether or not you are “winning,” look at whether or not you are going to hit your personal milestones. Perform a retirement assessment. How much do you need to retire? How much should you set aside (perhaps in index funds!) each month to reach that goal?

As long as you are on track to meet your goals, it doesn’t matter whether you beat the market — or your co-worker — at investing.

The worst thing you can do in any financial situation is compare yourself to others. Compare yourself to you and move forward.

5. I’m going to lose everything if the market crashes.

We all remember the market crash of 2008 and 2009.

It’s one of the reasons many of us are afraid to invest today. One of the most persistent investing myths is that you will lose everything during a market crash.

Do you know what I did when things looked ugly at the beginning of 2009?

I bought more shares of my favorite index funds.

For the most part, you only lock in your losses when you sell low. I stayed the course during the last couple of market events and even added to my portfolio. You get more bang for your buck when you buy during the dips.

While you’re young, you can afford to let it ride when you go through these crashes. As you get closer to retirement, you can consider moving some of your assets out of stocks and into bonds and/or cash. That way, your portfolio is somewhat protected close to the time you will actually need to start using that money.

But, for now, chances are that you can get through whatever the market throws at you.

There will always be down markets, bear markets, and crashes. Don’t react with panic and unload when you will guarantee losses.

Bottom line: investing is your best bet.

If you want to build long-term wealth, you need to get over the investing myths. Investing is your best bet for building financial independence in the future.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

At some point, there’s a chance that you’ll end up facing job loss.

Whether you are laid off, or whether you are fired, this can be a very challenging time. You have to worry about your finances, figure out what’s next, and hope that your job loss doesn’t negatively impact your search for a new job.

Being fired is a more serious situation than being laid off, unfortunately. The implication is that you did something very wrong — even if you feel like you didn’t deserve to be fired.

If you are facing job loss, this episode can help you figure out how to get back on your feet.

Concepts

The difference between being fired and being laid off.

How to find out why you were fired.

Illegal reasons for your job loss.

Do you qualify for unemployment benefits?

Tips for handling the situation when you are fired.

How to review your finances in the face of a job loss.

Tips for reaching out to your network to find a new job.

How to respond when you are being discriminated against or harassed.

This week’s “do-nows” focus on what you can take care of now — ahead of a job loss. Be on the lookout for discrimination, and always have your resume updated, just in case you are suddenly fired.

Become a Friend of Adulting

To get Adulting delivered directly to your device, subscribe using Apple Podcasts, Stitcher, Google Play, or your app of choice.

Once in a while, we present Adulting.tv LIVE! Stay tuned to hear about future events, and share your questions about or suggestions for our next discussions!

Disclosure: Adulting.tv may be compensated if you

take action after visiting certain links in this article at no cost to you. We stand by our editorial integrity and would not be linking to or discussing this topic if we didn’t believe it was in the best

interest of you, our audience.

What are the essential items you need to set up your first kitchen? If you’re on your own for the first time, this live podcast episode is essential for making the most of your money and creating a space that comfortable for cooking and gives you the opportunity to be successful in the kitchen.

Regardless of your cooking philosophy, Erin Chase will guide you through making the best decisions for stocking your first kitchen.

Lately, I’m not sure what’s going on with my money. Ever since getting back from three months of travel, I just haven’t felt like I have the time to sit down and see what’s going on.

This isn’t a healthy state of financial affairs.

I need to get real about my finances again.

Are your finances in shambles?

The first step to getting real with your finances is figuring out if they are in shambles. While my financial situation isn’t dire, I’m not exactly on top of money like I usually am.

However, I haven’t been tracking my spending like I usually do. Instead, I’m just sort of moving money around when I think I need to spend more. It’s a different approach than usual, and there are days that I feel like maybe I’m blowing through my monthly income faster than I should be.

If you’re keeping is real with your finances, you need to acknowledge your shortcomings. Have you been missing bill payments? Are you uncomfortable with your debt level? Do you spend without thinking about your purchases?

Look at your money situation and honestly acknowledge where you are. You can’t improve moving forward if you don’t know where you’re starting.

Evaluate your money goals.

Now that the new year approaches, it’s common to talk about setting goals. It’s an annual theme. And that includes goals about money. Once you know where you stand, you probably want to set goals that help you fix your financial problems or help you improve the situation for the future.

As you get real with your finances, it’s important to evaluate whether or not your goals make sense — and are realistic.

If you have a bunch of debt, it might not be practical to expect to pay it off in a few months. Maybe you can’t immediately max out your retirement account. There’s nothing wrong with this. Instead, the important thing is to make progress. Take a look at where you stand, where you want to be, and a realistic timeframe.

I know that I need to reconcile all my accounts for the last three months. I also need to review my own financial priorities and make adjustments since my new job. It’s a huge undertaking. I either need to suck it up and take a whole day to make it happen or I need to carve out smaller chunks of time over the course of a week.

Either way, I need to get real about my finances and about getting back on track.

Are you honest with your partner?

Let’s not forget that you need to keep it real with your finances when it comes to your life partner. In recent years, there are have been stories about financial infidelity, and the serious problems it causes over time.

No, this doesn’t mean that you need to combine your finances. In fact, I probably won’t combine finances with someone else again. However, I still need to be honest about my finances if I get with a potential partner.

I have a friend who keeps her finances separate from her husband’s. They don’t get into each other’s business. But they do generally keep each other updated about potential issues. You need to be honest about anything that could affect your relationship or the joint portions of your finances.

This might mean fessing up about your debt or admitting to your crappy credit score. It’s not the end of the world. But if you decide you want to buy a home together or if your debt could potentially put strain on your household finances, you need to be real about that.

It’s not easy, but it needs to be done.

When to keep your finances to yourself.

Keeping it real with your finances doesn’t mean that you go around telling everyone your money business. If you’re cool with that, there’s no shame in that game. However, don’t feel like you need to be completely transparent all the time.

I’m not someone who shares income reports. I don’t give exact numbers related to my student loan debt; I just say that I have it and don’t plan on paying it off early.

Even when you’re in a relationship you don’t need to share everything about your finances. I already know that I’m not telling someone about everything in my money life. I stay on top of my bills. I can afford what I spend my money on. I don’t have major issues that will sabotage any joint financial effort.

And that’s all anyone needs to know.

My parents don’t need to know exactly what I make. My friends don’t need to know my exact credit score. It just isn’t necessary.

There’s no reason to brag about your money, but you also don’t need to be ashamed to talk about some of your deals or address important issues.

As long as you own your financial situation to yourself and move forward to do what’s right with your money, you should be fine.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

If you had to come up with $500 for a car repair or a new appliance, could you get the money? What happens if you lose your job? It’s guaranteed that every adult will face some sort of emergency.

Don’t be one of them. Get ready for an unexpected setback by building an emergency fund designed to provide you with what you need in a pinch.

Concepts

What is an emergency fund, and why do you need one?

How much should be in your fund?

Where should you keep your emergency fund?

All-cash funds vs. keeping it elsewhere.

How to set up a tiered fund.

Tips for starting your emergency fund.

Characteristics of a good emergency fund.

Do credit cards have a place in an emergency?

Listen for our “do-nows” for specific actions you can take right now to begin building your emergency savings. We’ll also answer a listener question about how to free up money even when you’re sure you don’t have any available.

Become a Friend of Adulting

To get Adulting delivered directly to your device, subscribe using Apple Podcasts, Stitcher, Google Play, or your app of choice.

![[B011] Earn Money AND Do What You Love](https://adulting.tv/wp-content/uploads/2016/11/earn-money-do-what-you-love-1200x628.jpg)

![[A011 Rebroadcast] Scrooged: Don’t Be a Cheap Holiday Grinch](https://adulting.tv/wp-content/uploads/2015/12/a011-1200x628.jpg)

![[A049] Dump Debt or Invest: Choose Wisely to Avoid Destruction](https://adulting.tv/wp-content/uploads/2016/12/a049-1-1200x628.jpg)

![[A048] You’re Fired: Move Forward in the Face of Job Loss](https://adulting.tv/wp-content/uploads/2016/12/a048-1-1200x628.jpg)

![[B010] How to Set Up Your First Kitchen ft. Erin Chase, $5 Dinners](https://adulting.tv/wp-content/uploads/2016/11/your-first-kitchen-regular-1200x630.jpg)

![[A045] Ish Happens: Prepare For the Inevitable Emergency](https://adulting.tv/wp-content/uploads/2016/11/a045-1200x628.jpg)