Checkbooks are almost obsolete. But the old form of transferring money from one person to another is not quite ready to give up the ghost. Venmo might be fine for working out how to split the dinner check when you’re out with friends, and online bill pay definitely reduces headaches, but sometimes you have to pay a bill or put an initial payment down on a car, and you need to use a personal check.

File this under Essential Financial Skills for now. Having this skill makes you a financial bad-ass, or at least a budding financial bad-ass.

Checks come in books from companies that partner with your bank. Or you can order them separately for any checking account from independent checkbook companies. You can get fancy designs, which always cost money, or you can get a basic, traditional check design like the one I’ll use as an example here.

The fancy designs cost more. But whenever I open a new checking account, I make sure the bank will provide at least the first box of checks for free, if not free boxes of checks for the entire time I own the account.

Personal checkbooks usually have two options: single or duplicate. Duplicate checks just have special paper underneath each check that duplicates what you write so you have a record of it. That makes is easier to balance your checkbook and watch your finances.

The single checks assume you will remember what you paid, and they usually come with a check register. I always choose the duplicate checks because I find them more convenient when writing out a number of checks at a time, which I often do when I pay my bills.

Here’s an important piece of advice: Don’t write a check for money that you do not have in your checking account. Always track your finances so you know how much is available to pay. If you have $1,000 in your account and you know your $500 rent is about to be deducted from that account, you can’t write a check for $600 until you get more money.

Don’t try to beat the system thinking you’ll deposit more by the time someone cashes your check. Many checks are cashed electronically now and the money will disappear fast. It isn’t worth the overdraft fees or returned check fees.

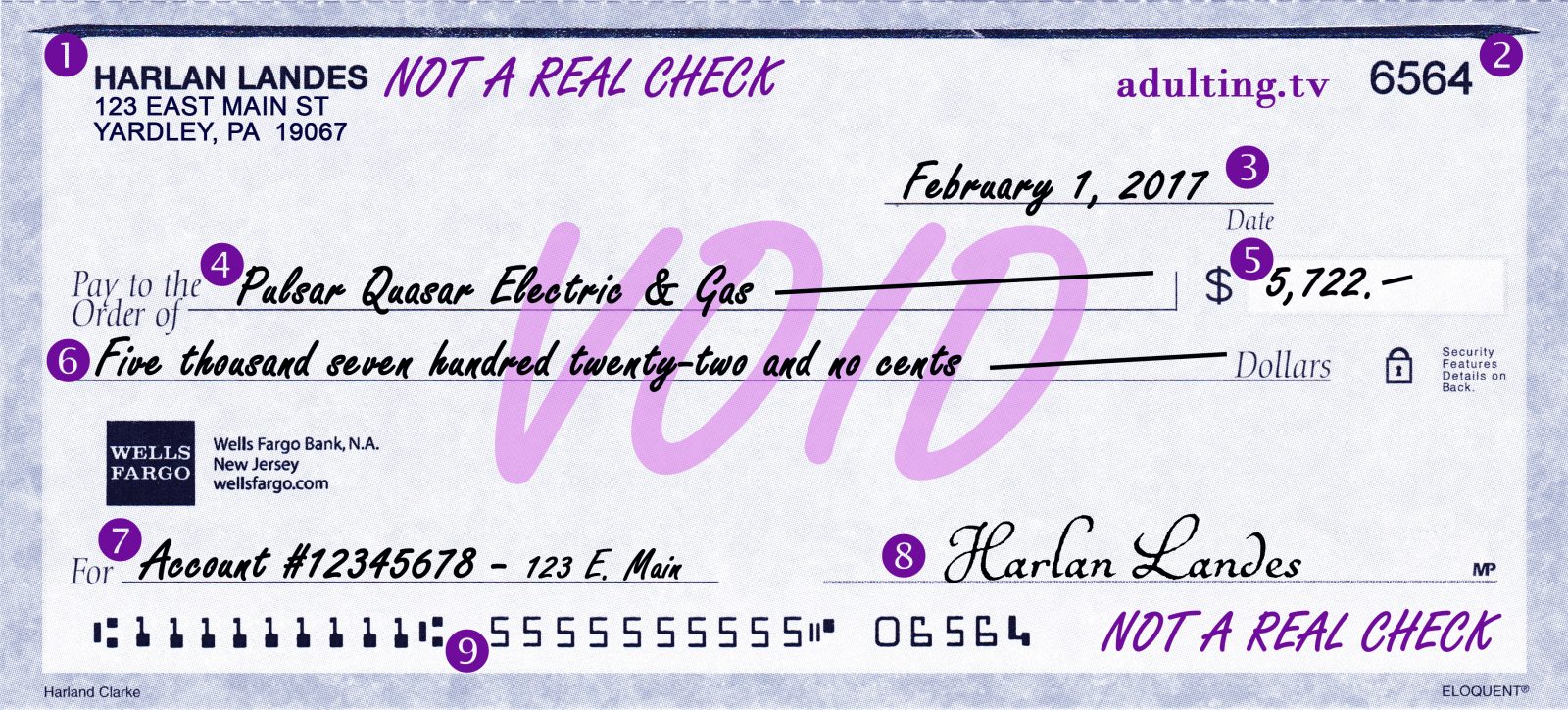

Here’s what a typical check will look like once you’ve written it out. Take a look at this sample and the explanations below. (Someone seems to have a sizable power service bill from the Pulsar Quasar Electric & Gas company.)

Cash me at da bank, how bow dah?

Naturally, your check won’t have “VOID” and “NOT A REAL CHECK” written on it. That’s just so no one’s inclined to try to use this graphic for any other purpose than as an example.

Here are the parts of the check as labeled above, and what you need to know about each section.

- Your address. If you ordered checks from the bank, this should be the address on your account. If you purchased checks separately, this will be whatever address you provided when you bought them. Make sure it’s accurate. But it will not hold up your money if it is incorrect. Some companies prefer you to also include your phone number, which you can write below your address or on the memo line (area 7) if you are so inclined.

- The check number. You should write your checks out in numerical order as much as possible. That makes it so much easier to tell, when looking at your bank statement or activity, if someone still hasn’t cashed your check.

- The date. When you write a check, put that day’s date here, and spell the month name out so there’s no chance of confusion. Pre-dating a check is when you write an earlier date. That’s completely unnecessary. If the company receives the check late, it’s still late, regardless of the date that’s written on the check. Post-dating is the opposite: writing a date that’s later than the current date. Some will do this when they know a deposit is coming and they don’t have money they need to cover the check in the bank account yet. Here’s the problem: any recipient can cash a check before the date that’s written on this line. Post-dating does not protect you. You could ask nicely and maybe the recipient won’t cash or deposit the check until the date you specify, but no one is required to wait. Big companies won’t. They’ll just ignore your post-dating attempt.

- The name of the recipient. This will either be a person’s name or a business name. Double-check the name, including the spelling. If the name is not correct, it can cause problems for the recipient when he or she (or the business) attempts to deposit it. Fill any blank space on this line with a line. This slightly helps prevent fraud, and I like to put a line wherever there is empty space.

- The dollar amount of the check. Write out the amount in Arabic numerals. If there are no cents, I like drawing a line as pictured above instead of writing the double-zero in 5,722.00. This is a personal preference.

- The amount of the check written out. Spell out the amount of the check. If you run out of space for the cents, you can draw a horizontal line and put the amount of cents all the way to the right above the line. Put two cross marks (exes) underneath the line. (See the second example below.) You don’t need to write the word “dollars” because that is already printed on the check. The word “and” should only be used in place of the decimal point in the amount.

- The memo line. Write something on this line that helps the recipient identify what that payment is for — or if you use duplicate checks, you can also use the memo line for a reminder for yourself. Some companies instruct you to use this for your account number or phone number.

- Your signature. Paper checks are not valid without your signature. Don’t forget to sign your check before you send it away or hand it to the person or company you’re trying to pay.

- Bank information. The number on the left is your bank’s routing (ABA) number. The next number on the bottom line of the check is your account number. Together, these two numbers identify your account and allow a bank to process your check. You should keep these numbers private, between you and the recipient only. The third set of digits is your check number. It should match the number at the top (indicated with a “2” in the example).

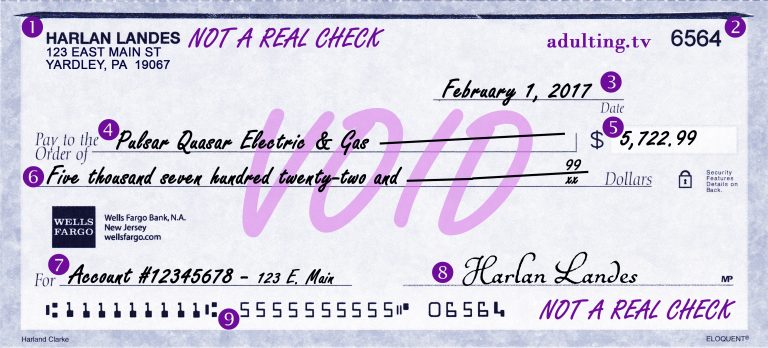

Here’s an alternative example without a round dollar amount, so you can see how the cents are written both in area 5 and area 6.

You have a number of options when writing amounts, and it doesn’t really make a difference exactly how you do it, as long as the amounts are absolutely clear, and the amounts in area 5 and area 6 match exactly.

If you don’t get checks for free through your bank account, you can order blank checks from any number of companies. Some of the most recognizable are Harland Clarke, Deluxe, and Checks Unlimited, but you can find more options on Vistaprint, Costco, and any number of other services and professional printers. You can even print your own.

Someday, paper checks will likely be eliminated from the banking system completely, but that’s a long way down the road. For now, even though they’re not as necessary in everyday life, you may still need to write occasional paper checks. Now you know what you need to know.

![[A057] You’re Covered: Choose the Best Health Insurance Plan](https://adulting.tv/wp-content/uploads/2017/02/a057-1200x628.jpg)

![[B013] How Couples Resolve Differences ft. Tai and Talaat McNelly, His and Her Money](https://adulting.tv/wp-content/uploads/2017/01/resolve-differences-1200x628.jpg)

![[A053] Winning at Money: Slay Your New Year’s Resolutions](https://adulting.tv/wp-content/uploads/2017/01/a053-1200x628.jpg)