Adulting.tv is a podcast featuring Harlan L. Landes and Miranda Marquit

Author: Harlan L. Landes

Harlan L. Landes is the founder of Consumerism Commentary, one of the first blogs about personal finance. He is a photographer and the founder and executive director of the Plutus Foundation.

This post may contain affiliate links.

Once you’re on your own, responsible for yourself, there’s no rule that says you have to figure everything about money out for yourself. Maybe you didn’t get into any good habits when you were growing up; maybe your parents didn’t guide you to making the best money choices.

Today, you start moving on the better path. Being an adult with your money boils down to five important steps you must take.

1. Open an investing account.

Think you need a lot of money to invest? You don’t. Without investing, it’s going to be really difficult to make the dreams you have for your life come true. If you want to work every day into old age and worry about how you’re paying the bills, you can get by without investing. But if you want something better for yourself, you need to get started today.

Start with an account at Betterment. Open an account today with as little as $30. You can save up first if you need to, but make this a goal for the end of the month. Betterment will guide you through your choices and help you pick the best investment for you. There’s no need to learn everything about stocks and bonds first. There will be time for that later — but by investing as soon as possible, you don’t miss out on the best aspects of the stock market: the gains.

2. Open a high-yield savings account.

Here’s what goes in your savings account: any money you don’t invest and don’t need to use to pay bills for the next month. Don’t just walk into your bank and open an account. Look at this list of the best savings accounts. The highest interest is important because a bank is just a place to store your money. You might as well make it work the hardest it can for YOU.

Talking about money with a partner is stressful! Make it easier with this free cheat sheet. This index card will help you talk about money without feeling nervous or anxious. Maybe you’re afraid to admit something, or maybe you’re concerned about what your partner will think. You can get through this, and your relationship will be stronger for it. Download the free cheat sheet by entering your email address below.

4. Increase your income.

Nothing is more satisfying when you create something and are paid for it. But there are many ways to get paid. And even if you have a day job, you should be exploring all the different ways to make some money on the side. At the same time, you need to focus on getting raises and promotions early in your career, because that has a huge effect on your lifetime earnings.

Even while increasing your job income, consider taking steps to make more money elsewhere. The latest hot tip is becoming an Uber driver. If you like spending time in your car, get paid to drive people around. It beats selling your body parts.

5. Get in those good habits.

While you want to focus on your money and the progress you’re making, the more you can automate some of the more helpful tasks, the better off you’ll be. Use direct deposit so you don’t have to worry about depositing your pay check. Here are some ideas:

If financial independence is the dream, financial stability is the first adult step along the path towards that vision.

On the final day of the year, fifteen years ago, I returned home from a weekend away to find my belongings on the lawn in front of the house I was renting. (I used the Internet Archive’s Wayback Machine to fact-check myself using my old, anonymous personal blog, my first time reading those entries in over a decade.)

My roommate thought I was moving out at the end of December, and when I wasn’t around, she moved two people into the room I had been occupying for several months. I had been planning to move out at the end of January, and the roommate knew this. But my name wasn’t on the lease, so perhaps she thought she could do whatever she wanted.

A later entry brought back the memory of a related event: I visited that apartment again ten days later to pick up a few remaining items, and the new occupants were moving out because that roommate committed some kind of check fraud. But I digress…

Being forced out of my living space with no notice on New Year’s Eve was the end of a particularly bad year. I lost a job, lost my car, and lost my girlfriend. I had moved to northern New Jersey for a job I no longer had. I was in my mid-twenties, but I wasn’t financially an adult. I survived by spending on credit cards, avoiding student loan bills, and accepting help from parents.

With the necessity of moving in with family as 2001 became 2002, I vowed to turn things around for myself.

I wasn’t necessarily aware of the idea of financial independence, but thankfully, that is how I can describe my situation today. In early 2002, I just wanted financial stability. And I had to figure out how to get there.

How I became financially stable.

After college, I chose a career somewhere between education and nonprofit. The organization I was working for was meant to be a stop-gap while looking for a teaching position, but I did enjoy it, and I didn’t put enough effort into moving forward. It cost me more to work as a nonprofit employee than I was earning — and I wasn’t even spending a significant amount of money.

1. I found a new job.

Instead of looking for my ideal career, my priority was earning money and getting back on my feet, taking control of my situation. Nothing is permanent. I could work on my loftier life goals while at least working somewhere during the day that would allow me the flexibility to plan for the future.

Without a car, I was limited to jobs that were accessible by walking or by traveling on the train. I turned to a technical temp agency. That’s how I earned money over breaks during college, and I knew I had many skills that would serve me well in corporate settings. I found something right away — an executive administrative assistant at a major financial firm.

This had no relation to my degree, but it was a job. And it paid 50 percent more than what I was earning at the nonprofit organization. Theoretically, I could even stay involved with the activity I was passionate about on weekends while working a “regular” job.

2. I designed a budget.

My dad helped me brainstorm a basic budget on the back of an envelope. That’s how I remember the situation. This budget had to take into account paying off a cash advance from my credit card, consumer spending on my credit card, and my student loans. I intended to move out and be less of a burden on family as soon as possible, so I budgeted for rent, as well. And savings for the future.

Partly because I wanted to stick to my budget and partly because I needed some self-reflection time to recover from bad choices, I also saved money in the first few months of my new job by staying in a fortress of solitude.

The budget was essential for setting myself up for financial stability.

3. I tracked every penny.

I used free software to meticulously track my spending, making sure I was staying within my budget and paying my bills on time.

You can only have a clear picture of where you’re going financially if you know where you are. It is incredibly easy today to get a full snapshot of your finances at any time thanks to technology. Apps communicate directly and securely with banks, so you all you need to do is check your phone to see where you stand. The app adds your bank balances and subtracts your debt, and the result is your financial net worth.

And beyond your net worth, you need to know how that changes over time, so you track your income and expenses, too. Today, I use Personal Capital and Quicken.

4. I started saving for the future.

It wasn’t enough to have a bank account whose balance was increasing every month. My new job offered a retirement plan with a matching contribution. Always say yes to a matching contribution. It’s free money.

How do you know when you’re financially stable?

To be considered financially stable — a true sign of adulting — you must meet these criteria.

You must be spending less than you’re earning. It doesn’t matter which side of the equation you try to improve, but it helps to focus on both your expenses and your income. You can only cut your expenses back so far — but income potential is unlimited. When you spend less than you earn, you have a surplus. The surplus allows you to have some control.

Living paycheck-to-paycheck — spending every penny you earn — means you have no surplus and you are not moving towards flexibility or control.

You don’t have to be debt-free, but you must be paying down your debt and not accumulating any more. If you’re able to make your minimum payments on your debt and then some, you’re in good shape.

You’re not relying on loans or gifts from family. This is the cornerstone of stability. You can make it on your own, just with your income and your expenses. It’s true that you may be in financial trouble if your income disappears, especially if you’re only beginning to establish savings, but for now, you are making it on your own.

You are building your future through savings and investment. Your nest egg might not be too big just yet, but it’s growing. You’re putting aside extra money to create an emergency fund and you have a systematic transfer to an investment account, preferably a low-cost index mutual fund.

Your friends support your goals. Don’t waste time around people who give you a hard time for being responsible. Often, when one starts acting more grown-up, the friends still wading through adolescence grow bitter. Or maybe you’re the last one to cross the threshold into actual adulthood.

People reach this point at different times in their lives. I wasn’t financially adulting until I was in my late twenties. Some start when they’re 40. And I’ve seen some sixteen-year-olds who are taking control of their future I never would have considered.

You’re moving forward steadily in your career. How you progress is often up to you, even when are faced with resistance was you’re trying to gain more responsibility, authority, and compensation at your job. You do know that often you have to accept more responsibilities before being granted more authority and increases in compensation. This type of success proceeds at different speeds, but you should always be aware of where you stand, and you make decisions that move you forward.

You have health insurance and you take care of yourself. Your health and well-being affect your ability to have a life of any sort in the future, so you watch your health and have an appropriate health insurance plan. You see a doctor once every one or two years, at least, if you’re otherwise healthy, and you see a dentist and dental hygienist every six months. If you need work, you get it done.

You pay your credit card balance in full every month.Credit cards can be great tools for people who are financially stable. They allow you to time-shift your spending, just like the DVR time-shifts The Walking Dead. They allow you to collect cash back and points that can be used for travel. But only if you avoid interest charges, late payments, and pay your balance in full every month.

This could be considered an “advanced technique,” and many people start messing with credit cards before they are prepared to handle the responsibilities. So watch out.

Financial independence is the next step after financial stability, but it could take a lifetime to achieve. Imagine if you no longer had to rely on your job. Imagine if you could live the life that you wanted to live, go where in the world that you wanted to go, and do anything that you wanted to do — without any concern about what the financial consequences would be.

That is financial independence. And you can’t get there without financial stability first.

Are you financially stable? If so, when did you finally achieve it?

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

With a real savings or checking account, you can handle emergencies and think about the future. Read More...

I understand the objections to owning a bank account, and I share many of the concerns. But proper adulting is nearly impossible without one of these best bank accounts, like it or not.

There may be some people in modern society who live a cash-only life, but that’s going to continue to get more difficult as time goes on unless they make many other sacrifices as well.

Why you absolutely need a bank account.

A bank account may be the only thing that gets you thinking about the future. When all of your mental energy is spent worrying about how you’ll make it through the week, you have no capacity for any kind of higher-order thinking. But that concern for the future is what is going to sustain you and your family over the long term.

Are any of these goals important to you?

Retiring from work and enjoying life all day instead of working until you die.

Buying a house.

Being able to support your children and eliminate unnecessary barriers for them.

Remaining calm when an emergency means you have to spend more money than you planned, sooner than you planned.

If at least one of these sounds appealing, start considering your future needs and saving for them.

Putting money aside is the gateway to flexibility. When you have access to cash, you have more choices. You have more freedom. It is the first step. It’s not enough to just save cash in your home. While it’s not a bad idea to stash some in case of emergencies, it’s dangerous to keep too much in your home or in your hand. It’s unprotected. It’s vulnerable. It could disappear, either by somebody finding it who shouldn’t, or by spending it when it would better for it to remain untouched for later.

Money in a bank account is safe. It will not disappear. In the many years of bank accounts being insured by FDIC, no one has ever lost money in a bank account. Even when banks fail — and some did during the latest recession — every customer had access to their money. The same cannot be said for cash hiding under the mattress or sitting on the shelf in a pickle jar.

Savings means the bank is working for you. When you deposit money, you are giving the bank the right to invest even more, and they often do by granting loans to community businesses and organizations. Banks earn money on these loans, and in general, some of that is passed onto you in the form of interest. Interest rates have been low lately, but those rates will eventually improve.

In the past, banks offered savings and checking accounts for free because they were making enough money from loans. As the depositor, your money is helping the bank earn a profit. But low interest rates have changed the situation, so now customers often have to shop around to find the best deals for bank accounts, but a free account shouldn’t be too hard to find.

There’s the ugly side of banking…

7 percent of households in the United States were unbanked in 2015, and that means that more than 15 million adults and more than 7 million children do not have access to a savings or checking account.

So how are these households, plus the more than 50 million adults and 16 million children who do own savings or checking accounts but are still considered underbanked, manage their money?

They use alternative services: check cashing at special storefronts or inside other retail stores like Wal-Mart, payday loans, pawn shop loans, and auto title loans. These services are expensive and tend to take advantage of individuals who feel they have no other alternatives.

… And there’s the uglier side of banking.

Why does it seem like the traditional banking route is no longer the best way to handle finances?

There never seems to be enough money.76 percent of Americans live paycheck-to-paycheck. After taxes, every cent is spent on things that seem necessary. Often, this means rent (or mortgage payment), food for the family, and basic utilities. That’s if a paycheck is coming in at all. Living on disability, Social Security, or unemployment results in even thinner income available for necessities — if any.

This is a difficult situation, and the lack of cash flow makes a bank account seem unnecessary, even if that’s not true.

The banks don’t behave well. Every week, there’s another news story about a major financial institution taking advantage of its customers. Wells Fargo just happens to be the latest bank to be caught in a scandal, opening accounts for customers without their knowledge.

The financial industry has a powerful lobby, and they will continue to make things difficult for customers for the benefit of their shareholders, and even the shareholders lose out in the end.

Credit unions don’t run into as many problems because there are fewer conflicts of interest. Credit unions don’t have shareholders, so any profit they may have finds its way back to customers — who are members — in some form.

You may not be able to open a traditional account. I look at my debit card, and it says I’ve been a customer since 1989. That means that an account has been open in my name since I was thirteen years old. My parents opened an account for me and showed me how to use a checkbook. (Neither debit cards nor ATM cards were widely available when big hair and pastels informed the zeitgeist.)

Not everyone has the benefit of financial role models. Those lacking are slower to build credit history and positive financial skills. Without a history in the banking system it’s difficult to get approved for that first account on your own, but it’s never too late or too early to take some steps forward.

Here’s what you can do right now.

Online bank accounts are the best options. If you’re comfortable buying items from Amazon.com online, you should be comfortable banking online. It’s more safe and secure than banking in person. Unfortunately, opening a bank account online often requires that you have an existing account to transfer money. There are ways to get around this, but it’s not easy.

Let’s go right to a bank or credit union first.

Find a credit union in your town. There are seven within five miles of my apartment, and that’s a fact I discovered by using the credit union finder at A Smarter Choice. An urban neighborhood nearby has more than 14. Take any cash you’ve collected recently and bring it in. Talk to a banker about your free options for checking and savings accounts.

When you have a real bank account, you break the cycle of paycheck-to-paycheck living. You begin thinking about the future. You stop wasting money on services like check cashing and short-term loans. You set yourself up for success. You set a good example for your family, now and for future generations.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

You could embarrass yourself and cause money problems if you screw up writing a check. Read More...

Checkbooks are almost obsolete. But the old form of transferring money from one person to another is not quite ready to give up the ghost. Venmo might be fine for working out how to split the dinner check when you’re out with friends, and online bill pay definitely reduces headaches, but sometimes you have to pay a bill or put an initial payment down on a car, and you need to use a personal check.

File this under Essential Financial Skills for now. Having this skill makes you a financial bad-ass, or at least a budding financial bad-ass.

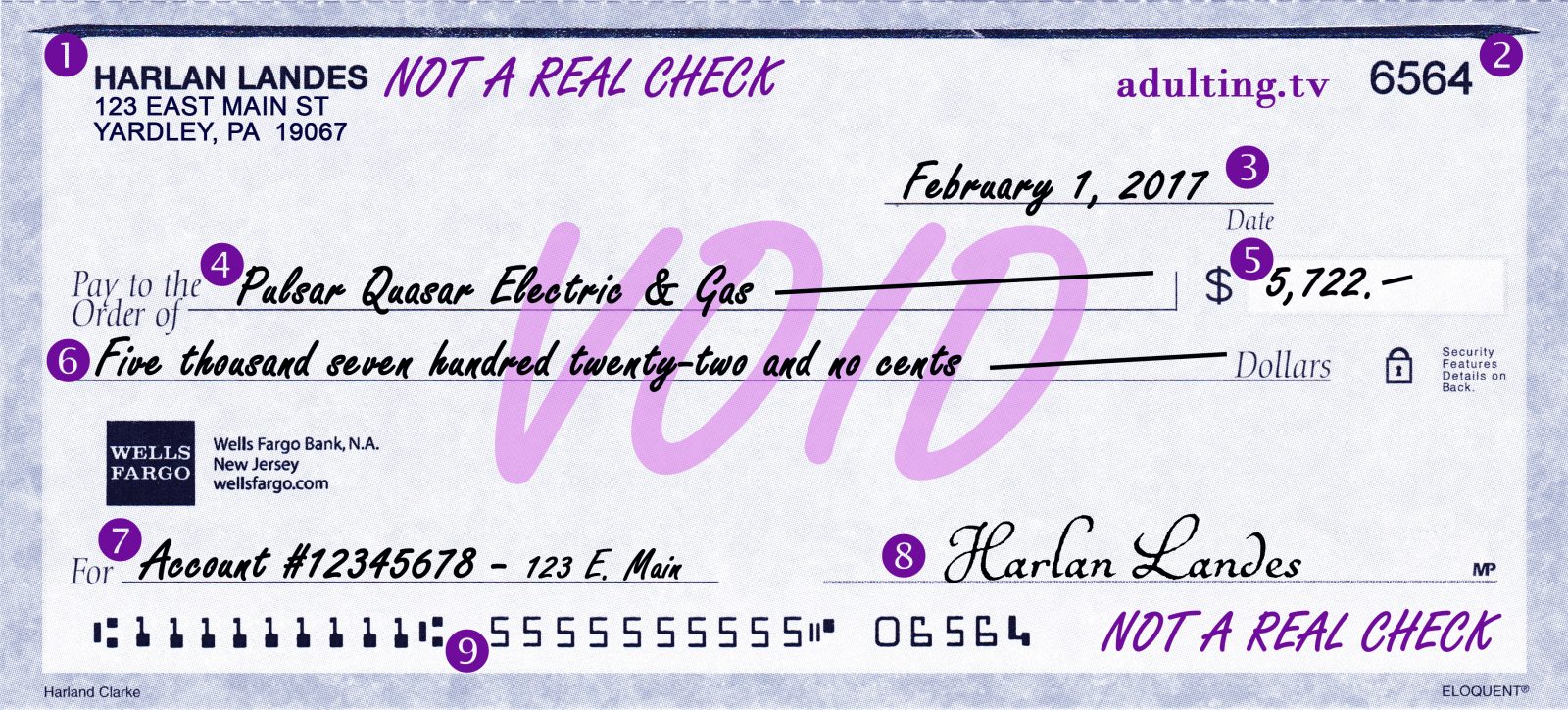

Checks come in books from companies that partner with your bank. Or you can order them separately for any checking account from independent checkbook companies. You can get fancy designs, which always cost money, or you can get a basic, traditional check design like the one I’ll use as an example here.

The fancy designs cost more. But whenever I open a new checking account, I make sure the bank will provide at least the first box of checks for free, if not free boxes of checks for the entire time I own the account.

Personal checkbooks usually have two options: single or duplicate. Duplicate checks just have special paper underneath each check that duplicates what you write so you have a record of it. That makes is easier to balance your checkbook and watch your finances.

The single checks assume you will remember what you paid, and they usually come with a check register. I always choose the duplicate checks because I find them more convenient when writing out a number of checks at a time, which I often do when I pay my bills.

Here’s an important piece of advice: Don’t write a check for money that you do not have in your checking account. Always track your finances so you know how much is available to pay. If you have $1,000 in your account and you know your $500 rent is about to be deducted from that account, you can’t write a check for $600 until you get more money.

Don’t try to beat the system thinking you’ll deposit more by the time someone cashes your check. Many checks are cashed electronically now and the money will disappear fast. It isn’t worth the overdraft fees or returned check fees.

Here’s what a typical check will look like once you’ve written it out. Take a look at this sample and the explanations below. (Someone seems to have a sizable power service bill from the Pulsar Quasar Electric & Gas company.)

Cash me at da bank, how bow dah?

Naturally, your check won’t have “VOID” and “NOT A REAL CHECK” written on it. That’s just so no one’s inclined to try to use this graphic for any other purpose than as an example.

Here are the parts of the check as labeled above, and what you need to know about each section.

Your address. If you ordered checks from the bank, this should be the address on your account. If you purchased checks separately, this will be whatever address you provided when you bought them. Make sure it’s accurate. But it will not hold up your money if it is incorrect. Some companies prefer you to also include your phone number, which you can write below your address or on the memo line (area 7) if you are so inclined.

The check number. You should write your checks out in numerical order as much as possible. That makes it so much easier to tell, when looking at your bank statement or activity, if someone still hasn’t cashed your check.

The date. When you write a check, put that day’s date here, and spell the month name out so there’s no chance of confusion. Pre-dating a check is when you write an earlier date. That’s completely unnecessary. If the company receives the check late, it’s still late, regardless of the date that’s written on the check. Post-dating is the opposite: writing a date that’s later than the current date. Some will do this when they know a deposit is coming and they don’t have money they need to cover the check in the bank account yet. Here’s the problem: any recipient can cash a check before the date that’s written on this line. Post-dating does not protect you. You could ask nicely and maybe the recipient won’t cash or deposit the check until the date you specify, but no one is required to wait. Big companies won’t. They’ll just ignore your post-dating attempt.

The name of the recipient. This will either be a person’s name or a business name. Double-check the name, including the spelling. If the name is not correct, it can cause problems for the recipient when he or she (or the business) attempts to deposit it. Fill any blank space on this line with a line. This slightly helps prevent fraud, and I like to put a line wherever there is empty space.

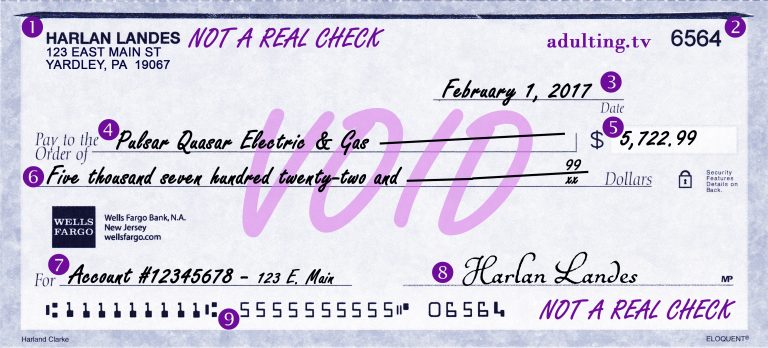

The dollar amount of the check. Write out the amount in Arabic numerals. If there are no cents, I like drawing a line as pictured above instead of writing the double-zero in 5,722.00. This is a personal preference.

The amount of the check written out. Spell out the amount of the check. If you run out of space for the cents, you can draw a horizontal line and put the amount of cents all the way to the right above the line. Put two cross marks (exes) underneath the line. (See the second example below.) You don’t need to write the word “dollars” because that is already printed on the check. The word “and” should only be used in place of the decimal point in the amount.

The memo line. Write something on this line that helps the recipient identify what that payment is for — or if you use duplicate checks, you can also use the memo line for a reminder for yourself. Some companies instruct you to use this for your account number or phone number.

Your signature. Paper checks are not valid without your signature. Don’t forget to sign your check before you send it away or hand it to the person or company you’re trying to pay.

Bank information. The number on the left is your bank’s routing (ABA) number. The next number on the bottom line of the check is your account number. Together, these two numbers identify your account and allow a bank to process your check. You should keep these numbers private, between you and the recipient only. The third set of digits is your check number. It should match the number at the top (indicated with a “2” in the example).

Here’s an alternative example without a round dollar amount, so you can see how the cents are written both in area 5 and area 6.

You have a number of options when writing amounts, and it doesn’t really make a difference exactly how you do it, as long as the amounts are absolutely clear, and the amounts in area 5 and area 6 match exactly.

If you don’t get checks for free through your bank account, you can order blank checks from any number of companies. Some of the most recognizable are Harland Clarke, Deluxe, and Checks Unlimited, but you can find more options on Vistaprint, Costco, and any number of other services and professional printers. You can even print your own.

Someday, paper checks will likely be eliminated from the banking system completely, but that’s a long way down the road. For now, even though they’re not as necessary in everyday life, you may still need to write occasional paper checks. Now you know what you need to know.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

The controversial Myers-Briggs Personality Type Indicator may not be perfect, but it’s fun. What’s your type? Read More...

You’ve seen the quizzes online. You may have even completed a personality assessment. I’ve taken this test many times since I was a teenager, and I’ve always received the same result. Consistency is just as good as accuracy, right?

This test is the Myers-Briggs Type Indicator (MBTI), or one of many adaptations. It’s designed to provide some insight to your personality type — a definition of how you tend to react in certain situations and possibly how you view the world.

Why do we care?

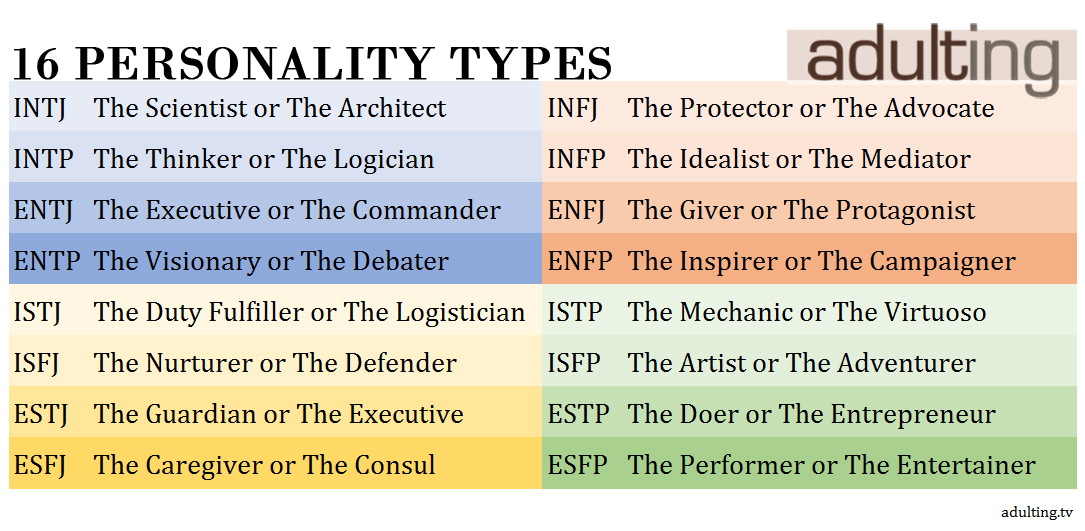

The test results are an effective icebreaker. When you know your type, as indicated by four letters representing four dimensions of personality traits, you have a shortcut to providing people you meet with a quick understanding of yourself. When an “INFP” meets an “ENFJ,” they each know a little bit more about each other. A little.

But it there any scientific proof that people fall into on of sixteen categories? It’s sketchy.

Does it matter? As long as you’re not using the results to guide decisions that affect people’s lives, there’s nothing wrong with a little entertainment.

This is huge in the corporate world.

The full Myers-Briggs evaluation goes into significant detail, well beyond the four assigned letters.

My work group, while I was working at an insurance company, spent two days taking the full evaluation, including “Step II,” and meeting with expert consultants to review how our personality types related to our interactions with co-workers and affected our ability to be productive for the company.

The consultants proctor a test that is supposedly more complete than the free online quizzes. They offer results that go into much deeper detail, primed for discussion about how we can all get along better in the office. Step II goes on to show how far on each dimension’s spectrum you happen to fall. For example, while I classify as “introverted,” it’s not an extreme identifier. I fall very close to the border between extraversion and introversion.

This is a lucrative industry for the Myers-Briggs Foundation, named after the two researchers who saw Carl Jung’s ideas about psychology almost a hundred years ago and dived deep into the subject (without any training in psychology — which was not as widespread a field of study as it is today).

For me the tests have been reliable, providing the same result (INFP, if you’re keeping track) time and time again, but I may have “learned” how to answer the questions in the test in such a way to produce that particular result. It’s not that hard to figure out.

Psychology Today points out that many self-evaluations like this produce unpredictable results. Its popularity endures because people like insight about themselves and others, and the MBTI conveniently categorizes (and generalizes) everyone into what appear to be sixteen distinct buckets.

The sorting hat has spoken.

Reviewing the category descriptions is like reading a horoscope or going to a fortune-teller. You’re bound to connect and resonate with some comments within your evaluation and say, “Wow! This totally sounds like me!” Here’s what one popular quiz has to say about my personality type, INFP, also known as “The Mediator” sometimes and “The Idealist” other times. “The Healer” shows up for INFP, as well.

INFP personalities are true idealists, always looking for the hint of good in even the worst of people and events, searching for ways to make things better. While they may be perceived as calm, reserved, or even shy, INFPs have an inner flame and passion that can truly shine. Comprising just 4% of the population, the risk of feeling misunderstood is unfortunately high for the INFP personality type – but when they find like-minded people to spend their time with, the harmony they feel will be a fountain of joy and inspiration.

Wow! This totally sounds like me! I have passion! I’m often calm and reserved! I always look for the good in people! I’m special and part of a select group! There’s a good chance it sounds like you, too.

INFPs like me would probably be sorted into Hufflepuff.

INFPs struggle with the issue of their own ethical perfection, e.g., performance of duty for the greater cause. An INFP friend describes the inner conflict as not good versus bad, but on a grand scale, Good vs. Evil. Luke Skywalker in Star Wars depicts this conflict in his struggle between the two sides of “The Force.” Although the dark side must be reckoned with, the INFP believes that good ultimately triumphs.

Wow! This totally sounds like me! I identify with Luke Skywalker!

Of course people are going to like and share the Myers-Briggs evaluation and results. Every single one of the 16 possible personality types focuses on positive traits and makes the tester feel good!

There is not one negative comment in any of the evaluations — and in real life, there are certainly negative personality traits that get in the way of collaboration and success.

The official MBTI experts call these definitions tendencies or preferences, not hard rules, so even if the descriptions don’t exactly represent one’s personality, they can still claim accuracy. If the Myers-Briggs Type Indicator is armchair psychology or even junk science, asking about someone’s type is still slightly better than asking about someone’s astrological sign. And learning anything about someone’s personality allows you to relate better to them. This is beneficial at work and helpful in your personal life.

Let’s break it down.

The first letter in the MBTI can be an I or E, and this represents extraversion. Like any of the dimensions in the evaluation, you can fall anywhere on the spectrum from “totally introverted,” through “something in the middle,” to “totally extraverted.” But these words don’t mean what you think they mean. To be extraverted means you draw your energy from socialization and being around and interacting with other people. Introverted people tend to be able to interact and socialize just as well, but need time alone afterwards to recharge.

The next dimension has “intuitive” on one side of the scale and “sensing” on the other side, represented by N or S. Those who tend towards sensing rely on information provided to them through their five senses to discover truth. Intuitive people go beyond sensory stimuli, finding patterns that reveal truth when interpreted.

In the third slot, the T stands for thinking and the F stands for feeling. You might as well ask someone if they’re “left-brained” or “right-brained,” because this is the same type of categorization. How do you make decisions? If you try to rely on logic most of the time, you’re a “thinker,” but if you go with your gut, you may be a “feeler.”

Finally, subjects are categorized into buckets that depend on whether they’re evaluated as “judging” or “perceiving” (J or P). Judging does not mean judgmental, but it does represent a preference for to-do lists, schedules, and closure. People with a perceiving preference are spontaneous and like having many possibilities open.

The result is sixteen unique combinations, and each has been given “names.”

Take the test.

Keeping the limitations in mind, you can still use a test to learn a little bit about your personality and get a morale boost if you’re feeling down. Understanding yourself is one of the keys to being a successful adult. Maybe it’ll be a good conversation starter. It probably won’t fully define you.

You and your closest friends may all share the same aspirations. Maybe it’s a beach vacation together, maybe it’s your own separate businesses, but you’re close because you share some kind of life goal and desire in common.

Squad goals started with those who, unlike Taylor Swift and her entourage, are outside of the mainstream and feed off the group encouragement and support from friends who face the same challenges from society.

But your squad goals are like your own goals. You have to put the time and the effort in if you want to see things happen. If your squad doesn’t have Taylor Swift or Waka Flocka Flame at the center, chances are you’ll all have to work equally hard.

Is your squad even healthy?

Before we get started, let’s address the fact that some groups of friendships aren’t entirely healthy. Your close friends or colleagues should be supporting each other, not secretly jealous and vindictive of each other. Leave the passive-aggressive behavior out of it.

Your crew should not be a clique, and you better not bully each other or other people. Get rid of any negative attitudes right now, before you decide to work on your squad goals.

Now, let’s start at the beginning.

What are your squad goals?

Vacations can be a blast when you go with your squad. If you’re going to get LIT, who else would you rather be with than your besties? I still dream about taking all of my friends on a cruise. One day, we’ll make that happen.

If some kind of trip is part of your squad goals, start planning now. Clear your calendars. Get recommendations for places to stay.

How about creating something? Have you and your closest friend always wanted to open a store to sell custom jewelry for toddlers? “Bling Babies” can still happen! Start the process: read some books and talk to store owners.

Are online businesses part of your group’s plans? Rather than working together on one plan, your squad goals could involve each of your friends working along on their own separate paths. With everyone working towards different goals, set aside some time to check in with each other. Support each other’s goals. Keep each other on track.

Everyone in the group can use their own skills, talents, and superpowers to help everyone else.

Being each others’ “accountability partner” is easy. So here’s the hard part: the money and the effort.

What do your squad goals cost?

Some goals take time and effort. Some take money. And a lot of goals take a combination of all of the above.

So when you plan, write down exactly what you need in order to make your dreams come to life. If the main requirement is time and effort, start prioritizing your life so you can bring your goals closer to you. Spend less time on things that matter less and more time moving you and your squad closer on the right path.

If money is the priority for living out your goals, take an honest look at where you are financially and where you need to be. If it’s far off, it could call for some drastic measures if you want to reach your goals within your own lifetime.

There are two sides to ending the day with more money. The first is the simpler of the two sides, but it may not always be the easiest. You just have to earn more money.

If you have a job, are you maximizing your income there? Can you take on more work to earn more cash? Have you asked for a raise recently? How about overtime?

Let’s say you’re maxed out at work. Do you take a second job? Make a career change? Start looking around for a new job that offers better incentives (like bigger paychecks)? You have to start considering these options.

The other side of growing your stash is being careful about spending. There’s only so far you can go before you’re living on the street, but maybe there are some expenses you can cut out. If you consciously make decisions about spending, keeping your squad goals in mind, you would be in a better place for keeping some money in your pocket.

So now that you’re saving money for your squad goals, how do you keep it organized and on track?

Open up a special bank account.

You could keep your squad-goal-money in a jar in your kitchen. But you’d probably be tempted to take some out once in a while for last-minute outings with your squad. Outings that have nothing to do with your real squad goals.

A safer place — safer from you and your own meddling — is the bank. Goal-oriented saving is the new thing for banks, especially those that are trying really hard to make their stodgy financial institutions more relevant to people like you.

We’ll list a few options here as examples. We’re not endorsing any company over any other. These companies are not advertisers or sponsors, so we are just sharing a couple that we have had experience with at Adulting.tv.

SmartyPig.SmartyPig was one of the first “banks” to offer a savings account in a way that is designed for goals. It’s not a bank itself, but it works with a bank behind the scenes. Sign up online and name your goal and the date you’d like to withdraw your money to spend for that goal. This is where I saved up for a camera for my photography business-slash-hobby.

Don’t worry, you don’t have to stick to the date or the goal if something in your life or your squad changes. Something always does, right? With all these accounts, you can take your money out at any time for any reason.

Capital One 360. Years ago, this account’s predecessor pioneered the idea of multiple savings accounts for different goals. You can put money into several accounts, and name each one after a specific goal. This is where I had my “emergency fund” and my “saving for a new car fund.”

That’s all you need. Not only will these places store your money until you’re ready to pay for making your squad goals happen, they’ll also pay you income. It may be just a little right now, but these are interest-paying accounts, so your balance will grow even without adding more of your own money in.

Pretty good deal, right?

Start saving now, and before you know it, you and your crew will be taking selfies on the moon. (How’s that for a squad goal?)

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

Start with this list. Focus on the essentials. Read More...

My last semester of college was during the fall months, and for the first time, I was living on my own, and not in a college dorm and not with my parents. No roommates, either, though that singular, private living situation wouldn’t last too long.

This apartment was a few miles off campus, past the entrance to the interstate highway, where rents were much cheaper. That’s exactly what I needed. My last responsibilities at college were student-teaching and preparing for my senior recital, the capstones to my music education degree. So I was still a student — a student without a job for at least a few months, without money being earned, and I don’t even remember how I was able to afford my rent.

The living situation was a big change from the dorm rooms in the preceding years. Everything is provided in the dorms — paid for along with tuition, naturally, but students never had to worry about outfitting rooms with basic furniture. At least a bed and a desk.

Somehow, I owned a bed and mattress. I have no memory of where they came from.

And that’s the only furniture I had in this apartment. Well, besides the bed, I had a television on the floor in the living room. I didn’t even have blinds or curtains on the patio door. If it didn’t come with the apartment, I didn’t have it. And nothing came with the apartment.

As a result, the place wasn’t exactly ideal for entertaining guests. I had no visitors so I wasn’t too concerned about the state of my domicile. All I needed to be able to do was sleep — which I did — and practice — which I sometimes did.

Maybe I had a lamp.

What would have been helpful to me is a guide that explains exactly what you need or should have in your first apartment, whether you have roommates or not.

Here is that guide. I’ve listed what you need, ranked in order of importance, by room. Many of the furniture items can be found on a budget. Always check second-hand stores or Craigslist.

You need these items for your bedroom.

1. Mattress. This is the most basic item. You need to be able to sleep relatively comfortably. A mattress will do the trick. If you’re on a budget, air mattresses can be quite comfortable these days, and much less expensive than a fancier typical mattress. A step up might be a futon. Unlike just about everything else, I would not buy this item on Craigslist or used at a thrift store.

2. Lamp. Shine some light in the bedroom. You’ll be thankful for illumination, especially in the winter when the sun sets early.

3. Alarm clock. Well, you probably have one on your smartphone. You may be living in your own for the first time and not sure how you’re going to pay rent, but I’m sure you’re managing your phone just fine. But having a real alarm clock as a back-up has saved me many times.

4. Window curtains. The one place where you don’t want neighbors peeking in is your bedroom. Maybe your place comes with blinds, and if so, curtains are further down on the list, but still good to have.

5. A bed. If you want to prop your mattress up a little higher than floor-level, you’ll need a bed. I lived in one apartment without a bed, though, so it is possible to get by without one.

You cannot have a bathroom without these.

1. Toiletries. Expect to brush your teeth every day. Grab all the basics including toilet paper, mouthwash, toothbrushes and toothpaste, soap, shampoo, shaving items, and a first-aid kit or at least adhesive bandages (Band-Aids).

2. Towels. Drip-drying takes far too long. You can get by with one, but two would be better. Feeling fancy? Get one of those towel hooks that fit over the bathroom door.

3. A shower curtain. Most apartments won’t come with one. Shower curtains can be inexpensive, and they give you privacy and added safety in the bathroom. You may need to buy curtain rings separately. You may even need to get your own curtain rod.

4. A plunger and toilet brush. One is for cleanliness and the other is to prevent a big mess.

Let’s go into the kitchen. Who’s cooking?

1. Dishware and silverware. No need to get fancy here. My first set was inherited from a friend. A few plates, a few bowls, forks, spoons, butter knives, and if you’re ready, a sharp knife set.

2. Pots, pans, a spatula, a ladle, a slotted spoon, a regular spoon, oven mitts, and a can opener. Unless you plan to order in every day and every night, you’ll be cooking. No need to get anything fancy here unless you really love spending time in the kitchen. Just the basics will suffice.

3. Dish soap, napkins, and paper towels. And if you have a dishwasher, dishwashing detergent.

4. Trash can. You need at least one in your apartment, and if you do have only one, it should go in the kitchen.

Not everyone has a living room, but here’s what you would need.

1. Something to sit in. In my first apartment, this was the floor. Somehow I managed, but it wasn’t ideal. You can find at least a cheap chair. I eventually upgraded — in my third apartment — to a cheap sofa from IKEA.

2. Curtains or blinds for the windows or patio/balcony door. Again, privacy is the main concern here, and some type of covering might be required by your lease.

3. A television stand or mount. These days, fancier people are mounting televisions on walls. In my first apartment, I got by with leaving the TV on the floor.

4. A coffee table. Again, I didn’t have one until later in my adult life, but this is a basic piece of furniture that separates the barely-adults from the mostly-adults.

Beyond these items, everything else could be considered a luxury. Chances are good that you won’t be in this apartment for a long time. You can upgrade and add items one at a time. Living in comfort is a process, and when you first move out on your own, there’s no expectation that you have the best-decorated and best-outfitted apartment among your friends.

Save the money now. Take care of your necessities and put away any cash you have left over. You can take your time and ignore the pressure to have everything in your life and your living environment together immediately.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

Whether in love or your career, whether you control it or not, you’ll probably pivot at least once in your life. Read More...

At some point during my third year of college, I started to suspect something wasn’t right. The path I set out for myself for the prior six years wasn’t quite satisfying me. A young man of many interests, the prospect of spending a lifetime focusing on being the best I could possibly be at one calling — teaching music — became unappealing.

Sure, teaching music is a wonderful path. The lasting impact teachers have on hundreds of lives is incomparable to most other roles and careers. I, however, felt strongly at that time that by following that typical career path and by putting as much of my life into my job as I expected would be necessary, I wouldn’t have the kind of fulfillment I was looking for.

My first major pivot.

While in college, I pivoted my approach. After several attempts to fit a minor course of study into my schedule, I settled on a minor focused on nonprofit. It was a pivot that I now see as a good move because it helped shape the projects I take on today and gave me more paths towards living a life of doing important things.

The pivot is the key to not just success but survival. If you’re a professional athlete, focus on sharpening your broadcast skills so you have an opportunity for a “second act” once you can no longer compete — especially if you aren’t one of the few superstar athletes who could publish a memoir people would buy.

If you run a business, a pivot could be revolutionary. It’s a fundamental change in the nature or strategy of the company. Nintendo is known for video games and gaming technology, but the company launched in the 19th century making vacuum cleaners and playing cards. The executives saw the birth of a trend very early on, and in 1966, turned to video games and never looked back.

It was a massively successful pivot.

There’s nothing more pivotal than the life of a serial entrepreneur. Take one business to a certain point, exit that business through a sale or merger, and move onto the next project. In the same vein, I’ve seen people develop successful businesses, and once they’ve gone as far as they’d like to go, they’ve begun their next business selling other entrepreneurs on the ideas that led them to their initial success. “You, too, can be a success, just like me! I’ll tell you how. Buy my e-book and take my online course!”

Adaptability is the key to a successful pivot.

Adaptability is one of the most important adult skills. If you’re too set in your ways and not amenable to change, you can be guaranteed that life will pass you by, and if you’re after happiness, it may prove to be elusive. You’ve got to be paying attention to today’s trends, predicting the future, and have a keen awareness of your skills.

Tim Tebow’s now a baseball player. A podcast company called Odeo became Twitter. Jessica Alba went from actor to entrepreneur — and if that’s not a complete pivot, at least it’s diversification.

Pivots in your personal life can be even more monumental. Moving out of a toxic relationship could be the best pivot for your long-term health and happiness. The list of famous relationship pivots is too long to include here.

Pivot successfully with five steps.

Here’s how you can prepare for a successful pivot, and you can expect to have at least one major pivot in your life — more if you want to be as agile as possible, increasing your changes for success and happiness.

Are you ready to make a pivot in your life or career? These are five important steps.

1. Focus on being a generalist with as much enthusiasm as a specialist.

Take the time to explore your interests and learn about related areas. Although people no longer tend to work for the same company from the moment they can work to the moment they retire (or die), there still is a strong trend to stay in the same field. Often, a strong career requires a highly specialized degree, and that education takes a long time.

But a great education prepares students for adapting to the world, whatever it might bring. Use time in college to experiment with different paths, especially if you are talented in or passionate about a variety of fields. Gain experience working in areas you wouldn’t normally consider. Practice solving problems of all types.

There’s a danger when people become experts or become immersed in a narrow field. So many mortgage brokers — trained to be nothing more and without other marketable skills — found themselves out of work during the credit crunch period of the last recession.

Multi-faceted experience gives you a level of employability first of all, and beyond that, the potential to take your income into your own hands through building your own business, consulting, freelancing, or otherwise honing in on entrepreneurship.

2. Open your mind to new ideas.

It’s possible you discover an important pivot by saying yes to interesting opportunities. While it’s important not to distract yourself from the job you are doing, closing yourself off to signs that the world is changing around you will be disastrous.

Find interesting people — or anyone doing work in something that interests you — and ask questions. Get acquainted. Learn from them.

3. Guide yourself by a broad vision.

Corporate mission statements are often specific, and direct a company towards the type of work they do. Sometimes these mission statements change, but the overall vision remains the same.

Your vision should be broad. What kind of world do you want to live in? The answer to that can be your vision. And when you pivot, even if it’s from one career path to another, it can still fit in with your vision of the future.

But don’t feel bad if it doesn’t. You’re allowed to change your mind. You’re allowed to follow a path that has no relation to the journey you started. That’s an inherent benefit of being an adult.

4. Predict the future.

Easy right? It’s not impossible. You don’t have to be a fortune teller to get it right. You just have to pay attention to the little details, and have a good grasp on human behavior, using history as a guide.

Keep an eye on the world around you, because that’s how you can learn to spot minute changes that signal the shape of the future. For example, not many people accurately predicted the latest economic recession with significant advance warning, but once the recession was apparent, it was relatively easy to figure out what some of the world’s biggest concerns and trends were going to be in the coming years.

5. Plan your pivot as much as possible.

If you want to jump into the pool’s deep end, you should probably know how to swim first. If you don’t know how, you may struggle, and your basic need for survival may be the only force preventing you from drowning. Maybe.

Prepare with knowledge and practice, and your chance for survival increases. Reduce the risk of the pivot by doing research, talking to others who have made similar moves, and setting up your personal support system.

Your support system includes friends and family who want to see you succeed with the changes in your life. There will always be doubters, though. You may want to ignore them and remove negativity from your life, but that’s not always the best idea. Even critics might have a perspective worth considering — not all, but some.

But you do need people who will cheer you on and provide moral support.

Create a timeline. And depending on whether you like the sink-or-swim challenge, either you give yourself no option but to keep trying until you succeed, or give yourself a back-up plan. Build that into your timeline, but don’t be afraid to adjust or adapt — or pivot — as the needs arise.

Whether it’s part of your plan or appearing by surprise, your life will include at least one pivot. Take control of your pivot with preparation and planning, and be ready to pivot at any moment. Look for the opportunities.

You never know what kind of success or happiness is out there if you move only in one direction and ignore your peripheral vision.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

If you want to nail that next job interview, follow these 8 expert job interview tips. Read More...

Everything’s on the line when you go in for a job interview in person. You’re under pressure whether to earn money to keep food on your family’s table or to go as far as you can with your first job. The initial job interview for the position is your chance to make a great first impression and solidify your likelihood for employment.

Whether you get a call back for a second interview, you get offered the job on the spot, or your follow-up calls are ignored is somewhat up to you.

Prepare for the interview far in advance.

1. Be aware of the purpose of the interview from your perspective. You’re looking for a job. Companies are looking for employees. You’re not going to be a good match for every opportunity out there, and that goes both ways. The interview is a chance for you to find out if a company is right for you.

If you desperately need a job, you may be willing to accept an opportunity that isn’t a good fit. Interviews are successful when no one is desperate, and the pressure is off to accept an offer. You should use the opportunity as a chance to evaluate the company you may be spending years of your life with and the people you’ll interact with every day.

Go to the interview with the attitude that you’re not going to settle.

2. Approach your interview like an audition. Your meeting is a test of your communication skills. Practice like you would for an audition. Ask your successful friends to role-play the interview.

Go on interviews for jobs you don’t intend to accept. This isn’t a waste of time; it’s excellent practice for meeting people and communicating about yourself, even if the details will be different for every interview.

3. Learn everything you can about your role and the people interviewing you. Do your research. You should enter the interview with a wealth of knowledge about the company.

The focus of this knowledge depends on the type of job you’re seeking and the level at which you expect to be hired, but be ready to communicate about the strengths, weaknesses, opportunities, and threats (SWOT) you expect to encounter in your role.

4. Examine your public profile. Any company seriously considering a job candidate will do their own due diligence on you. Your reputation will need to survive a criminal background check as well as cursory social media investigation. This is where always maintaining a professional image online can help you.

The first step is controlling what you publish publicly online. Don’t be stupid by sharing with the world anything that you wouldn’t want seen in an article about you in the New York Times.

Next, you have to think about what your friends are posting about you.You have little control over what your friends do, and most reasonable employers recognize that social media isn’t necessarily a professional settings, but items shared by your friends can reflect poorly on you and your reputation.

Take care of this on the day of the interview.

5. Get sleep, arrive early, look the part. You should be at your best to make a positive first impression. Be relaxed and healthy, and a good night’s sleep before the interview can make a big difference.

Plan to arrive early for the interview. If you do arrive early, you will have a chance to look around and get comfortable with your surroundings. Planning to arrive early also gives you a buffer of time, and that will come in handy if a train or bus is running late or if there’s a traffic jam on the way to your appointment. Even when your lateness is due to something beyond your control, it reflects poorly on you.

Know ahead of time what you’re expected to wear while on the job, and choose an outfit a little nicer.

6. Project a positive attitude during the interview. For the purposes of the interview, you have a better chance of getting a job offer if your attitude matches what the hiring manager or your interviewer expects. There are a number of variables at play for these expectations, and there can be subtle or major differences based on sex.

Regardless of sex, confidence is the most appealing personality attribute during an interview. But confidence must be carefully controlled. Not everyone who is confident is doing a good job of presenting themselves, especially if that confidence is interpreted as superior or demeaning to others.

Express your confidence in a way that makes everyone in the room feel good about themselves.

Along with confidence, honesty and humility go far, especially when there’s a strong desire to prove yourself to be the best. You are human — be yourself.

7. Ask intelligent, relevant, and surprisingly bold questions. Inevitably, every interviewer provides the job applicant with an opportunity to ask questions. By this point in the interview, you’ve probably done a great job answering questions about your experience and expressing who you are while in the hot seat.

Have you sprinkled well thought-out questions as you go along? Doing so helps shift the focus around during the interview and allows you to find out more about the position and the company. Even still, it’s good to have a few questions in your back pocket for that one opportunity you know will come at the end of the interview. This isn’t the time to ask about vacation days or your 401(k) vesting schedule.

Assuming you’ve already asked all the relevant questions throughout the interview, the end is a good chance to show your bold side. Ask if the interviewer has any reservations or concerns about what you’ve said during the interview — or anything that might prevent the company from offering you the job. This does two things:

If the answer is no, you’re solidifying the interviewer’s interest in you by making them affirm it out loud.

If you did say something the interviewer didn’t like, you’ll get a chance to address the concern and clarify yourself. This can turn a “no” into a “yes.”

Don’t drop the ball after the interview.

8. Promptly follow-up with a thank you note. Some companies take longer to process applicants than others. The hiring process might be long. You don’t want to pester your potential manager, but you do want to make sure they are reminded of your interest.

A thank-you note within 24 hours of the interview, sent by email, is generally accepted to be a polite follow-up. Be sincere and thank your interviewer for the opportunity and their time. You may even want to use this as an opportunity to ask an additional question about the job, just to keep the communication going.

But don’t be alarmed if you don’t receive a reply. The lack of reply likely has nothing to do with you. There may be any number of other applicants, and the manager might be busy. You’ll hear from the company if and when they’re ready to move to the next stage of the hiring process.

Good luck with the interview. Regardless of the outcome, keep a positive attitude and don’t burn your bridges.

Like what you’ve read?

Join other #adults who receive free weekly updates.

For a limited time you’ll receive our new book, The Best Bank Accounts for Adults, when you sign up!

How do you know when it’s the right time for sex, especially with a new partner? Read More...

Adults can have sex whenever they both decide that they want to have sex, if everyone involved is capable of consenting, and if doing so would be legal.

Providing those two conditions are met, feel free to make your own choices about physical intimacy. But not so fast — at least not at first. The best decision is an educated decision, so there are some things you should know first about yourself and your partner, covering your attitudes, values, beliefs, and approaches to any consequences.

The decision to have sex may seem a little more complicated if it would be your first time with a particular partner — or first time overall. Give the following considerations some thought before taking a relationship to the next level of intimacy or adding sex where there may be no relationship at all.

Sex can even be an impulse decision if you’ve already gone through the process.

What is important to you?

Do you feel that you need to have a emotional connection with a partner before starting any physical intimacy? The first thing to think about is what you value in a relationship and what kind of beliefs you have. Your beliefs may be influenced by your parents, the community you grew up in, or input from other people around you. Everyone’s situation is somewhat different.

The first step is communicating your beliefs and your values surrounding relationships to your partner. You do not have to have the same opinions, but it helps to understand where the other is coming from. This goes a long way towards avoiding any emotional surprises later on.

You might even find that you think you feel one thing, but you find that later on, you change your mind, or you feel that your initial feelings were wrong. It’s good to recognize that as a possibility, regardless of how you feel today.

What type of relationship, if any, is important to you before you have sex? Do you want to act on purely physical arousal? Would you prefer to have an emotional connection before Netflix and chill? Or do you consider yourself a sapiosexual — a word I just recently learned — turned on by intelligence? There’s no right answer; it all comes down to what you like.

And if you don’t know what you like yet, you should feel free to experiment, make mistakes, and figure it out. On that note…

Do you feel pressured?

You shouldn’t let anyone pressure you. The decision to have sex is one you need to have the freedom to come to on your own first, then as a couple. Don’t allow your partner to manipulate you, make you feel guilty, or convince you to do something you’re not ready for. Communicate honestly about your desires, and expect the same from your partner. Trust goes a long way to making sure the sex you do have is enjoyable and fulfilling — and potentially amazing!

Pressure can come from outside the couple, too. Your friends may not be pressuring you outright or on purpose, but you might feel pressure just being within a group of friends who have a different approach to sex than you do. Try to separate your image of yourself from the idea of what you think people expect from you.

You could be pressured into not having sex, too. Keep in mind that as an adult, you have the freedom to say yes. It can be difficult to remember this if you have been receiving opposite messages consistently and repeatedly from people you trust since adolescence. Physical intimacy is not bad, evil, or inappropriate. It can be risky, but it shouldn’t be shameful.

A question I hear often is regarding the number of dates with the same person after which sex is expected. Sex should never be expected. You should wait until you feel you’re ready to be intimate with that particular partner. The number of dates is irrelevant.

How would you handle the consequences?

Starting or continuing a physically intimate relationship can have unintended consequences, so it’s best to think about what you would do personally in the event of each consequence, and then talk about what you would do as a couple.

If the relationship involves a man and a woman, pregnancy is a potential outcome. Have you given any thought to what you would do or how you would feel if you or your partner becomes pregnant as a result of your intimacy? Have you discussed this? And if not, are you taking enough precautions to try to prevent the situation? And then what happens if the preventative measures fail?

How familiar are you with your partner’s sexual history? And beyond history, what about the present? Are you both sleeping with other people as well? Basic information about other sexual partners is helpful to prevent the spread of STIs. Combine this knowledge with safe, protected sex, and you are setting yourself up for healthy sex. Condoms will help protect both against pregnancy and STIs, while birth control via pill, patch, implant, or some other means will only help avoid pregnancy. But there are no guarantees.

And while it may not be as important as these considerations, you might need to think about the well-being of others beyond your potential sex partner. Are either of you in emotional or physical relationships with others? How will your actions affect your other relationships?

Sometimes, the consequences might be nothing more than feeling awkward when seeing your partner under normal circumstances. Sometimes, even people who think they can handle being friends with benefits find that they’re uncomfortable around the other person or even develop a stronger emotional connection when they weren’t planning to. These consequences can be frustrating or they can be great — depending on whether everyone involved continues to share the same attitude and feelings towards the relationship.

The role of sex in a relationship.

Sex can strengthen a good relationship or add excitement outside of a relationship. It doesn’t solve all the problems throughout the world, and in fact, it can also harm others if it’s included in an abusive relationship. Avoid using sex as a bargaining chip or to control your partner’s behavior. But there are no rules other than what the law calls for, including the ability to consent.

Sex is meant to be fun! It’s all about pleasure and enjoying each other. If it doesn’t feel good, change something, don’t be nervous, avoid the pressure, and keep trying.